Understanding the Building Blocks of Your Claim’s Value

When an accident leaves you injured, one of the most pressing questions often surfaces: What is the true value of my personal injury claim? While many factors contribute to this assessment, accurately projecting future medical expenses is often the cornerstone of a fair and comprehensive valuation. These costs, stretching from emergency care to long-term rehabilitation, represent not just bills but a significant portion of your future well-being.

When an accident leaves you injured, one of the most pressing questions often surfaces: What is the true value of my personal injury claim? While many factors contribute to this assessment, accurately projecting future medical expenses is often the cornerstone of a fair and comprehensive valuation. These costs, stretching from emergency care to long-term rehabilitation, represent not just bills but a significant portion of your future well-being.

We understand that navigating the complexities of a personal injury case valuation can feel overwhelming. That’s why we’ve put together this guide. We will explore how medical cost projections are carefully calculated. We will also see how they integrate with other damages like lost wages and pain and suffering. Finally, we will cover the critical role they play in securing the compensation you deserve. Understanding this vital component is essential for maximizing your claim and ensuring all your future needs are met, playing a crucial role in any comprehensive Richmond personal injury valuation.

After an accident on a busy road like I-95 or Broad Street, understanding your claim’s value is crucial. It begins with knowing the types of compensation, or “damages,” you can pursue. These damages are designed to make you “whole again” after suffering an injury due to another’s negligence, as much as monetary compensation can allow.

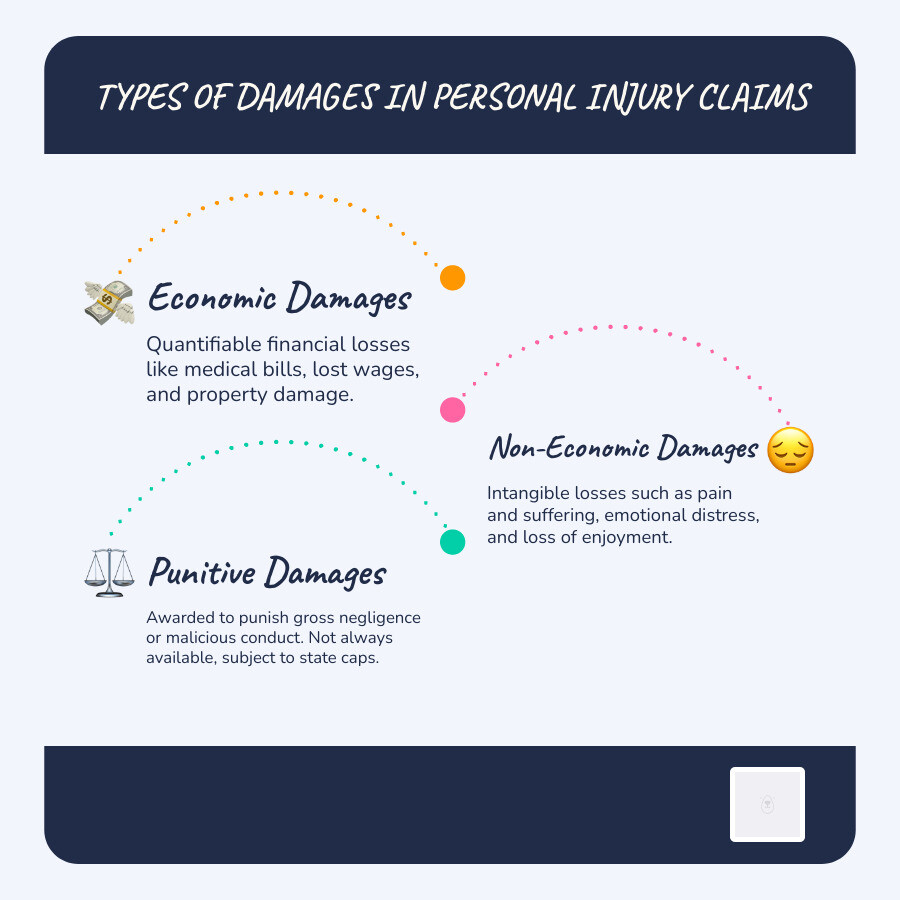

Economic vs. Non-Economic Damages

The legal system generally categorizes damages into two primary groups: economic and non-economic. This distinction is fundamental to understanding how a personal injury claim is valued.

Economic Damages (Special Damages): These are the tangible losses, often easily quantifiable with receipts, bills, and pay stubs. They represent direct financial costs incurred as a result of the injury. Examples include:

- Medical bills: Emergency care, doctor visits, hospital stays, surgeries, prescription medications, physical therapy, rehabilitation, and assistive devices.

- Lost wages: Income lost due to time off work for treatment or recovery. This can include past lost income and, crucially, future lost earning capacity if the injury impacts your ability to work long-term.

- Property damage: Costs associated with repairing or replacing damaged property, such as a vehicle in a car accident.

- Other out-of-pocket expenses: Transportation to medical appointments, home modifications for accessibility, domestic services you can no longer perform yourself, and other miscellaneous costs directly related to your injury.

Non-Economic Damages (General Damages): These are the intangible losses, which are much harder to quantify because they don’t come with a bill or an invoice. They represent the subjective impacts of the injury on your life. Examples include:

- Pain and suffering: Physical discomfort, chronic pain, and the overall physical anguish experienced due to the injury.

- Emotional distress: Psychological impacts such as anxiety, depression, fear, anger, PTSD, and other mental health challenges arising from the accident and its aftermath.

- Loss of enjoyment of life: The inability to participate in hobbies, recreational activities, or daily routines that once brought joy and fulfillment.

- Loss of consortium: Damages awarded to a spouse for the loss of companionship, affection, and sexual relations due to the injured partner’s condition.

- Disfigurement and scarring: Compensation for physical alterations that impact self-esteem and quality of life.

While non-economic damages are harder to calculate, they are frequently the most significant portion of a potential personal injury claim, especially in cases involving severe or long-lasting injuries. Insurance companies commonly use a multiplier formula, multiplying medical expenses by a factor (e.g., 1.5 to 5 or more for severe cases) to estimate these general damages.

What Are Punitive Damages?

Beyond compensatory damages (economic and non-economic), there’s a third, rarer category: punitive damages. Unlike compensatory damages, which aim to reimburse the injured party, punitive damages are intended to punish the defendant for particularly egregious or reckless conduct and to deter similar behavior in the future.

Punitive damages are typically awarded only in cases where the defendant’s actions demonstrate gross negligence, malicious intent, or a conscious disregard for the safety of others. For example, a drunk driving accident that results in severe injuries might warrant punitive damages, as the act of driving under the influence shows a reckless disregard for human life.

Punitive damages are not always awarded, and state laws often impose caps or strict criteria for their application. They are an exception rather than the norm in personal injury claims, but when applicable, they can significantly increase the overall value of a case.

The Cornerstone of Valuation: Projecting Medical Costs

The journey toward a fair personal injury settlement often hinges on one critical element: medical expenses. These costs can be extensive, encompassing not only immediate emergency care but also a lifetime of potential treatments. Accurately projecting these costs is fundamental to a fair valuation, especially for injuries treated at major medical facilities.

Calculating Current and Future Medical Expenses

When an accident occurs, the immediate medical needs are often clear: emergency care, ambulance rides, and initial hospital stays. However, a comprehensive valuation must look beyond these immediate costs to encompass the full spectrum of necessary care.

Current Medical Expenses: These are the costs already incurred, including:

- Emergency room visits and urgent care.

- Hospitalization and surgical procedures.

- Diagnostic tests (X-rays, MRIs, CT scans).

- Doctor visits and specialist consultations.

- Prescription medications.

- Physical therapy, occupational therapy, and rehabilitation services.

- Medical equipment (crutches, wheelchairs, braces).

Future Medical Expenses: This is where the valuation becomes more complex and critical. For many serious injuries, the path to recovery is long, and some conditions may never fully resolve. Future medical expenses can include:

- Ongoing physical or occupational therapy.

- Future surgeries or medical procedures.

- Long-term medication needs.

- Regular doctor visits and specialist care.

- Home healthcare or assisted living.

- Psychological counseling for emotional trauma.

- Adaptive equipment or home modifications.

A key concept in this area is Maximum Medical Improvement (MMI). This is the point at which a patient’s condition has stabilized, and further medical treatment is unlikely to result in significant improvement. Once MMI is reached, medical professionals can better assess the long-term prognosis, including any permanency of the injury. This permanency can lead to residuals, which describe ongoing or future treatment a person might need, such as continuous therapy, in-home nursing, or a wheelchair.

To ensure all these costs are adequately accounted for, specialized expertise is often required. Professionals skilled in creating detailed personal injury cost projections can provide comprehensive reports that outline all anticipated medical needs and their associated expenses, providing a robust foundation for your claim. These projections are vital for ensuring that you are not left with out-of-pocket expenses years down the line.

The Impact of Injury Severity on Personal Injury Case Valuation

The nature and severity of your injuries are paramount in determining the value of your personal injury claim. Not all injuries are created equal in the eyes of the law or insurance adjusters.

“Hard” Injuries vs. “Soft Tissue” Injuries:

- Hard injuries are those that are objectively verifiable through medical imaging or clinical findings, such as broken bones, dislocations, torn ligaments, or internal organ damage. These injuries tend to be valued higher because their existence and severity are less debatable.

- Soft tissue injuries, like whiplash, sprains, and strains, affect muscles, tendons, and ligaments. While very real and often debilitating, they can be harder to objectively prove and may be viewed with more skepticism by insurance companies, potentially leading to lower valuations. This makes thorough documentation and consistent medical treatment even more crucial.

Objective vs. Subjective Findings:

- Objective findings are medical observations that can be measured or seen by others, such as a fracture on an X-ray, swelling, or a visible laceration.

- Subjective findings are symptoms reported by the patient, such as pain, numbness, or dizziness. While subjective complaints are valid, objective evidence strengthens a claim significantly.

Long-Term Disability, Scarring, and Disfigurement: Injuries that result in long-term disability, permanent impairment, or significant scarring and disfigurement carry a higher valuation. These conditions impact a person’s life indefinitely, affecting their ability to work, engage in daily activities, and maintain their self-image. For instance, a severe burn that leaves permanent scars or an injury that necessitates a lifelong reliance on a wheelchair will command a much higher settlement than a temporary sprain. The valuation of scarring, in particular, can be complex, sometimes requiring years to fully assess its impact as the healing process evolves.

The more severe and lasting the injury, the greater the economic and non-economic damages, and thus, the higher the potential value of the personal injury claim.

Key Factors That Adjust Your Claim’s Value in Richmond

A simple calculation of medical bills and lost wages is rarely enough to determine the true value of a personal injury claim. Several legal and practical factors can significantly increase or decrease the final settlement amount, especially in a state like Virginia.

Liability and Virginia’s Contributory Negligence Rule

One of the most critical factors influencing a claim’s value is liability – who was at fault for the accident. If the other party is clearly 100% at fault, your claim stands on strong ground. However, if there’s any question of shared fault, the waters become murky, particularly in Virginia.

Virginia operates under a strict legal doctrine known as contributory negligence. This rule is notoriously harsh and differs significantly from most other states. In a contributory negligence state, if you, the injured party, are found to be even 1% responsible for the accident, you are completely barred from recovering any compensation, regardless of how negligent the other party was. This means that even minor actions on your part could entirely derail your claim.

For example, if an at-fault driver runs a red light and hits you, but it’s determined you were marginally speeding, under contributory negligence, you could lose your entire case. This rule is also followed in a handful of other states, such as Maryland and North Carolina, as well as the District of Columbia. In contrast, most states follow some form of comparative negligence, where your award is merely reduced by your percentage of fault.

The strictness of Virginia’s contributory negligence rule makes the importance of evidence paramount. Establishing clear liability and demonstrating that you were not at fault is crucial for any successful claim in the Commonwealth.

How Policy Limits and State Laws Impact Recovery

Even with a strong case and clear liability, external factors can limit the potential recovery in a personal injury claim.

Insurance Policy Limits and Defendant’s Assets: The amount of compensation you can ultimately receive is often capped by the at-fault party’s insurance policy limits. If the damages exceed these limits, collecting the full amount can become challenging. Unless the defendant has significant personal assets that can be pursued, the available insurance coverage often dictates the maximum realistic recovery. This is where your own underinsured motorist (UIM) coverage can become invaluable, stepping in to cover damages beyond what the at-fault driver’s insurance pays.

Damage Caps: Some states impose statutory limits, or “caps,” on certain types of damages, particularly non-economic damages (like pain and suffering) or punitive damages. While Virginia does not have a general cap on non-economic damages in most personal injury cases, it does have a cap on damages in medical malpractice cases, which can significantly impact the value of such claims. It’s essential to understand the specific laws that apply to your case.

Statute of Limitations: This is a critical deadline that sets the maximum time frame within which you can file a lawsuit after an injury. In Virginia, the general statute of limitations for most personal injury cases is two years from the date of the injury. Missing this deadline almost certainly means losing your right to pursue compensation, regardless of the merits of your case. The approaching statute of limitations can also influence settlement negotiations, potentially leading to lower offers as the deadline nears.

Collateral Source Rule: This rule, which varies by state, determines whether the defendant can reduce their payout by the amount you received from other sources, such as your health insurance. In some states, like Rhode Island and Massachusetts, the Collateral Source Rule prevents insurance companies from offsetting what they owe by money received from third-party sources. Virginia generally follows a modified version of the collateral source rule, allowing the plaintiff to recover the reasonable value of medical services, even if a portion was paid by insurance or written off. Understanding this rule is important for calculating the full value of medical expense compensation.

These legal and practical considerations underscore why a thorough understanding of the law and careful strategic planning are essential for maximizing your personal injury claim.

Putting It All Together: A Guide to Richmond Personal Injury Case Valuation

Calculating the total value of a personal injury claim involves combining all damages and carefully adjusting for the various factors we’ve discussed. This process is more of an art than a science, requiring a comprehensive analysis that considers both quantifiable losses and subjective impacts.

Here’s a simplified breakdown of the steps involved in determining a potential settlement range:

- Tally Economic Damages: Add up all current and projected medical expenses, lost wages (past and future), property damage, and other out-of-pocket costs.

- Estimate Non-Economic Damages: Use common methods (like the multiplier) to assign a monetary value to pain and suffering, emotional distress, and loss of enjoyment of life.

- Adjust for Fault: Apply the state’s negligence rules (e.g., Virginia’s contributory negligence) to reduce or bar recovery based on your percentage of fault.

- Consider Policy Limits and Other External Factors: Account for the at-fault party’s insurance limits, your own UIM coverage, and any state-specific damage caps.

Common Methods for Estimating Claim Value

Insurance companies and attorneys typically use a combination of methods to arrive at an initial estimate for a personal injury claim:

- Multiplier Method: This is one of the most widely used methods, particularly for estimating non-economic damages. It involves taking the total economic damages (especially medical expenses) and multiplying them by a factor, or “multiplier,” which typically ranges from 1.5 to 5. For severe, long-lasting, or particularly painful injuries, the multiplier can be even higher. The choice of multiplier depends on factors like the severity of the injury, the length of recovery, the impact on daily life, and the clarity of liability.

- Per Diem Method: Less common but still used, especially for pain and suffering, this method assigns a daily monetary value to the injured person’s pain and suffering for each day from the date of the accident until they reach Maximum Medical Improvement (MMI). This daily rate might be based on the injured person’s daily income or a reasonable figure for daily discomfort.

- Damage Calculation Software (e.g., Colossus): Many insurance companies use proprietary software programs, such as Colossus, to help them estimate claim values. These programs input various data points about the accident, injuries, medical treatment, and other factors to generate a suggested settlement range. While these tools aim for consistency, their algorithms are often closely guarded trade secrets, and they frequently produce lower valuations than what a jury might award. It’s crucial to remember that these are tools for insurers, and their output should not be taken as the definitive value of your case.

- Role of Expert Witnesses: For complex cases, expert witnesses play a crucial role in valuation. Medical experts can provide detailed prognoses and justify future medical costs. Vocational experts can assess lost earning capacity. Accident reconstructionists can clarify liability. Economists can calculate the present value of future losses. Their testimony and reports provide objective evidence that significantly strengthens a claim’s valuation.

Understanding these methods is key to navigating the negotiation process. The initial figure derived from these methods often represents the settlement value – the amount an insurer is willing to pay to avoid the risks and costs of going to trial. The trial value, on the other hand, is the potential amount a jury might award if the case proceeds to court, which can be higher but also carries greater uncertainty. A thorough understanding of these dynamics is part of a comprehensive personal injury claim assessment.

The Role of Legal Guidance in Personal injury case valuation

Given the complexities of personal injury law, the intricacies of medical cost projections, and the strategic maneuvers of insurance companies, legal representation is not just beneficial—it’s often essential.

An experienced personal injury attorney brings invaluable expertise to the valuation process:

- Gathering Evidence: Attorneys know what evidence is needed to prove liability and damages, from police reports and medical records to witness statements and expert testimony.

- Hiring Expert Witnesses: They have a network of medical, vocational, and economic experts who can provide credible testimony and detailed reports to support your claim, especially concerning future medical costs and lost earning capacity.

- Navigating Contributory Negligence: In Virginia, an attorney’s skill in demonstrating that you were not at fault, even minimally, is critical to overcoming the strict contributory negligence rule.

- Negotiating with Adjusters: Attorneys are accustomed to the tactics used by insurance adjusters and can effectively counter lowball offers, negotiate for a fair settlement, and ensure all aspects of your damages are considered. They understand the nuances of the multiplier method and how to argue for a higher multiplier based on the specifics of your injury and its impact on your life.

- Maximizing Settlement Offers: By carefully calculating all damages, presenting a compelling case, and being prepared to go to trial if necessary, an attorney can significantly increase the chances of securing the maximum possible compensation for your injuries.

While online calculators offer estimates, accurately valuing a case requires professional assessment to consider all components, including obscure or future costs, and to account for the unique legal landscape of your jurisdiction.

Frequently Asked Questions about Personal Injury Case Valuation

Can I accurately calculate my own case value?

While online calculators and general formulas can provide a rough estimate, accurately calculating your own case value is extremely difficult and often leads to undervaluation. These tools cannot account for the complexities of a case, such as Virginia’s strict contributory negligence rule, the nuances of future medical needs, the subjective nature of pain and suffering, or the strategic negotiation tactics of insurance companies. A professional assessment by an experienced personal injury attorney is necessary to ensure all components of your claim are considered, helping you avoid settling for less than your case is truly worth.

How is compensation for pain and suffering determined?

There is no exact, universally applied formula for determining compensation for pain and suffering (non-economic damages). However, attorneys and insurers often use methods like the “multiplier” or the “per diem” as a starting point for negotiations. The multiplier method typically involves multiplying your total medical expenses by a factor (e.g., 1.5 to 5 or more, depending on severity). The “per diem” method assigns a daily rate for your suffering from the injury date until Maximum Medical Improvement (MMI). The final value for pain and suffering is highly subjective and depends heavily on factors such as the severity and type of injury, the duration of recovery, the impact on your daily life, the strength of your evidence, and the jury’s tendencies if the case goes to trial.

How long does it take to settle a personal injury case?

The duration of a personal injury case settlement can vary significantly, from a few months to several years, depending on numerous factors. Straightforward cases with clear liability and minor injuries might settle relatively quickly, perhaps within a few months. However, complex cases involving severe injuries, disputed liability, extensive medical treatment, or significant future damages can take much longer, potentially several years, especially if a lawsuit becomes necessary. Reaching Maximum Medical Improvement (MMI) is a key milestone that often precedes final settlement negotiations, as it allows for a more accurate assessment of all damages, including future medical costs and permanency.

Conclusion

Determining the true value of a personal injury claim is a detailed, multi-faceted process that goes far beyond adding up initial bills. It requires a deep understanding of legal principles, medical prognoses, and negotiation strategies. By understanding the core components of damages, the critical role of future medical cost projections, and the impact of state-specific laws like Virginia’s strict contributory negligence rule, you can better understand the potential worth of your claim. Securing fair compensation for your injuries means carefully accounting for every loss, both tangible and intangible, and being prepared to advocate for your rights.