Introduction: Why Legal Guidance is Crucial in Times of Family Turmoil

A family crisis can turn our world upside down. Whether it’s a sudden loss, a serious accident, or an unexpected illness, these events bring immense emotional distress. The last thing we want to think about then are complex legal matters.

Yet, these crises often come with urgent legal and financial questions. Ignoring them can lead to bigger problems down the road. We might face issues like securing assets, managing legal documents, or making official notifications. Getting the right legal guidance after crisis moments is key to protecting our loved ones and our future.

This guide will walk you through the essential steps to take. We will explore how to secure physical and digital assets, what institutions to notify, and common legal problems that arise in different crisis scenarios. We will also discuss the vital role of legal counsel in these challenging times, emphasizing the need for expert assistance, such as Board-Certified legal guidance after crisis, to ensure your family’s best interests are protected. Our goal is to help you steer these complexities with confidence and clarity.

Immediate Legal Steps to Take Following a Family Crisis

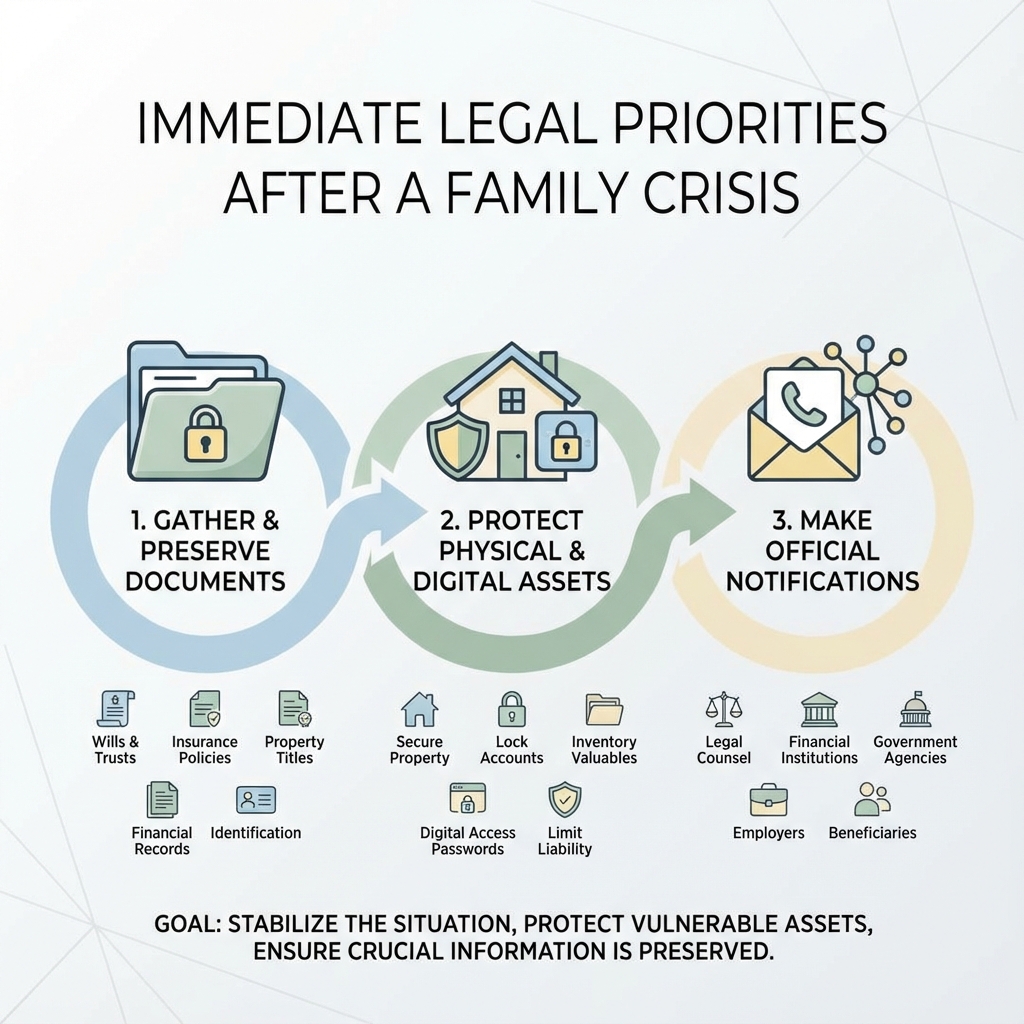

When a family crisis strikes, the initial shock can make it difficult to think clearly. However, taking immediate legal steps is paramount to safeguarding your family’s interests and laying the groundwork for recovery. Our priority in these moments is to stabilize the situation, protect vulnerable assets, and ensure that crucial information is preserved. This often begins with a focused effort on document gathering, asset protection, and making necessary official notifications.

Securing Physical and Digital Assets

One of the most critical immediate steps is to secure both physical and digital assets. This prevents unauthorized access, loss, or misuse during a chaotic period.

Physical Assets:

- Bank Accounts: If a loved one has passed away or become incapacitated, immediately identify all bank accounts (checking, savings, investment). Notify the banks of the situation and inquire about procedures for freezing accounts or transferring access, depending on the circumstances and your legal authority (e.g., power of attorney, executor appointment).

- Real Estate: Secure any properties owned by the affected individual. This might involve changing locks, ensuring utilities are maintained, and preventing unauthorized entry. If the property is vacant, inform neighbors or arrange for regular checks.

- Vehicles: Ensure vehicles are safely parked and secured. If the owner is incapacitated or deceased, determine who has legal authority to operate or manage them.

- Valuables: Identify and secure any physical valuables like jewelry, art, or important documents stored in the home or safety deposit boxes.

Digital Assets: In our increasingly digital world, securing online accounts is just as vital:

- Online Accounts: This includes email, social media, banking portals, investment platforms, and e-commerce sites. Accessing these may require legal authority, but identifying them is a crucial first step.

- Passwords: If accessible, gather passwords for critical accounts. If not, understand the recovery processes for each platform.

- Preventing Unauthorized Access: Be vigilant about potential identity theft or fraud. Monitor credit reports and bank statements for unusual activity. Consider placing a fraud alert or credit freeze.

A comprehensive list of essential documents to locate and secure includes:

- Will and Trust Documents: These are foundational for estate administration.

- Life Insurance Policies: Critical for financial support.

- Deeds and Property Titles: Proof of ownership for real estate.

- Bank and Investment Statements: Overview of financial holdings.

- Tax Returns: Provide a snapshot of financial history and assets.

- Medical Records and Bills: Essential for health-related crises and insurance claims.

- Birth, Marriage, and Death Certificates: Necessary for various legal processes.

- Digital Asset Inventories: A list of all online accounts and platforms.

Effective communication with family members is also key. Designate a primary point of contact to avoid confusion and ensure everyone is informed about the steps being taken.

Notifying Key Institutions

Prompt notification to relevant institutions is essential to manage the legal and financial fallout of a family crisis. Each institution has specific procedures and requirements.

- Social Security Administration (SSA): If there has been a death, the SSA needs to be notified promptly. They can provide information on survivor benefits and other entitlements.

- Financial Institutions: Banks, credit unions, and investment firms where the individual held accounts must be informed. They will guide you on accessing funds, changing account ownership, or settling debts.

- Insurance Companies: Notify all insurance providers, including life, health, auto, and home insurance. Understand the claims process and required documentation.

- Employers: If the crisis involves an employee, notify their employer. This is important for benefits, final paychecks, and any workplace-related support.

- Credit Bureaus: Inform credit bureaus (Experian, Equifax, TransUnion) of a death to prevent identity theft and fraudulent activity.

- Utility Companies and Service Providers: If a property will be vacant or needs services adjusted, contact utility companies, internet providers, and other service providers.

Navigating these notifications can be overwhelming, especially during emotional distress. We recommend keeping a detailed log of all communications, including dates, names of individuals spoken to, and summaries of discussions. This meticulous record-keeping will prove invaluable as you proceed.

Common Legal Problems in Different Crisis Scenarios

Family crises manifest in various forms, each presenting its own unique set of legal challenges. Understanding these common problems can help us anticipate issues and seek appropriate legal guidance after crisis events. Whether it’s dealing with the aftermath of a sudden death, a severe accident, or a loved one’s incapacitation, proactive legal engagement is crucial.

After a Sudden Death: Estate and Probate Challenges

The death of a loved one is a profoundly difficult experience. When it’s sudden, the emotional toll is compounded by the immediate need to address legal and financial matters. The process of settling an estate, known as probate, can be complex and time-consuming.

- Locating a Will: The first critical step is to determine if the deceased had a valid will. This document outlines their wishes regarding asset distribution, guardianship of minor children, and executor appointments. If no will is found, the estate will be settled under the laws of “intestate succession,” meaning state law dictates how assets are distributed, which may not align with the deceased’s unspoken wishes.

- Executor Duties: If a will exists, the named executor is responsible for managing the estate. Their duties typically include:

- Filing the will with the probate court.

- Notifying heirs and beneficiaries.

- Taking inventory of all assets (real estate, bank accounts, investments, personal property).

- Paying legitimate debts and taxes.

- Distributing remaining assets to beneficiaries according to the will or state law.

- Asset Inventory and Debt Settlement: This involves a meticulous accounting of everything the deceased owned and owed. Assets may include bank accounts, investment portfolios, real estate, vehicles, and personal belongings. Debts can range from mortgages and credit card bills to medical expenses. The executor must ensure all creditors are properly notified and paid before beneficiaries receive their inheritance.

- Beneficiary Distribution: Once all debts and taxes are settled, the remaining assets are distributed. This process must strictly adhere to the terms of the will or the laws of intestacy. Disputes among beneficiaries can arise, particularly if the will is unclear or if there is no will, leading to potential litigation.

- Understanding the Court Process: Probate is a court-supervised process. The level of court involvement varies by state and the complexity of the estate. It can involve multiple filings, hearings, and strict deadlines. Navigating this without experienced legal counsel can be daunting. For comprehensive assistance and probate guidance after crisis, seeking specialized resources can simplify this often-overwhelming process.

Following a Serious Accident or Injury

A serious accident can lead to life-altering injuries, significant medical expenses, and an inability to work. The legal aftermath involves intricate processes to determine liability and seek compensation.

- Insurance Claims: Immediately following an accident, dealing with insurance companies becomes a primary concern. This includes your own insurance (e.g., health, auto, homeowner’s) and potentially the at-fault party’s insurance. Insurers often aim to minimize payouts, making it crucial to have legal representation.

- Liability Determination: Establishing who was at fault is central to any personal injury claim. This involves gathering evidence from the accident scene, police reports, witness statements, and expert analysis. Clear determination of liability is essential for successful compensation.

- Medical Records and Lost Wages: Comprehensive medical documentation of injuries, treatments, and prognosis is vital. This evidence substantiates the extent of damages, including current and future medical costs, rehabilitation, and pain and suffering. If injuries prevent you from working, documentation of lost wages and future earning capacity is also crucial.

- Seeking Compensation: Compensation in personal injury cases can cover medical expenses, lost income, property damage, pain and suffering, and emotional distress. The goal is to restore the injured party to their pre-accident condition as much as possible, or to compensate them for permanent losses.

- Statute of Limitations: It is critical to be aware of the statute of limitations, which is the legal deadline for filing a lawsuit. This varies by state and type of claim. Missing this deadline can permanently bar you from seeking compensation. Given the complexities of accident claims and the need for timely action, securing experienced legal counsel for personal injury cases is highly advisable. Such counsel can provide invaluable support in navigating these challenges.

When a Loved One Becomes Incapacitated

The incapacitation of a family member due to illness or injury presents profound legal, financial, and emotional challenges. Planning for such an event, or responding to it, requires careful legal consideration.

- Power of Attorney (POA): A durable power of attorney allows a designated agent to make financial decisions on behalf of an incapacitated individual. A medical power of attorney (or healthcare surrogate designation) grants authority for healthcare decisions. Without these documents in place, managing a loved one’s affairs can become extremely difficult.

- Healthcare Directives/Living Wills: These documents express an individual’s wishes regarding medical treatment, especially end-of-life care. They guide medical professionals and family members in making decisions consistent with the patient’s values.

- Guardianship Proceedings: If a person becomes incapacitated without a valid power of attorney or healthcare directive, family members may need to petition the court for guardianship (sometimes called conservatorship). This is a legal process where a court appoints a guardian to make decisions for the incapacitated person (the ward). Guardianship can be a lengthy and expensive process, often involving court hearings and ongoing reporting requirements.

- Conservatorship: Similar to guardianship, conservatorship typically refers to the court appointment of someone to manage the financial affairs of an incapacitated individual, while guardianship may cover personal and medical decisions.

- Managing Finances and Care: Whether through a POA or guardianship, the appointed individual takes on significant responsibility for managing the incapacitated person’s finances, paying bills, overseeing investments, and ensuring they receive appropriate medical care and living arrangements. This role demands meticulous record-keeping and often involves navigating complex healthcare systems and financial regulations.

These scenarios underscore the profound need for timely and expert legal guidance after crisis events. The stakes are incredibly high, affecting not just financial well-being but also personal autonomy and family harmony.

The Role of Legal Counsel: Your Advocate for Legal Guidance After Crisis

In the wake of a family crisis, emotions run high, and the path forward can seem obscured by grief, confusion, or anger. This is precisely when the objective, experienced hand of legal counsel becomes indispensable. A lawyer acts as your advocate, protecting your rights, offering sound advice, and navigating the often-complex legal landscape on your behalf. Their role extends beyond mere paperwork; they are strategic partners in securing your family’s future.

Legal professionals bring a critical perspective to situations fraught with emotion. They can:

- Protect Rights: Ensure that your legal rights and those of your family are upheld, preventing exploitation or disadvantage during vulnerable times.

- Objective Advice: Provide unbiased, clear advice based on legal principles, helping you make informed decisions without the cloud of emotional distress.

- Negotiation: Skillfully negotiate with insurance companies, creditors, opposing parties, or other family members to achieve fair settlements and resolutions.

- Litigation: Represent your interests in court if a dispute cannot be resolved through negotiation, guiding you through court procedures and legal strategy.

- Court Procedures: Manage all aspects of court filings, deadlines, and appearances, ensuring compliance with legal requirements.

- Legal Strategy: Develop a comprehensive legal strategy custom to your specific situation, aiming for the most favorable outcome.

When to Engage an Attorney for Legal Guidance After a Crisis

While it’s often beneficial to consult an attorney early in any crisis, certain situations particularly demand immediate legal engagement. Delaying can lead to missed deadlines, loss of crucial evidence, or irreversible mistakes.

- Complex Estates: If a deceased loved one had a substantial estate, multiple beneficiaries, significant debts, or a business, an attorney specializing in estate law is essential to steer the intricacies of probate and asset distribution.

- Contested Wills: When family members dispute the validity of a will or the distribution of assets, legal counsel is necessary to mediate, negotiate, or litigate the matter in court.

- Catastrophic Injuries: Accidents resulting in severe, long-term, or permanent injuries require an attorney experienced in personal injury law. They can accurately assess damages, negotiate with insurers, and pursue litigation to secure adequate compensation for medical care, lost income, and quality of life.

- Insurance Disputes: If an insurance company denies a claim, offers an unreasonably low settlement, or acts in bad faith, an attorney can challenge their decisions and fight for the coverage you deserve.

- Unclear Liability: In accidents where fault is disputed or multiple parties might be responsible, a lawyer can investigate, gather evidence, and establish liability to protect your claim.

- Guardianship Needs: When a loved one becomes incapacitated without proper legal documents (like a Power of Attorney), initiating guardianship or conservatorship proceedings requires legal expertise to ensure the court appoints the most suitable person and that the incapacitated individual’s best interests are protected.

Navigating Insurance and Contracts with Legal Guidance After a Crisis

Insurance policies and existing contracts become critical documents during a crisis. Understanding their terms and implications is vital, and legal guidance after crisis situations can be the difference between a successful outcome and significant financial loss.

- Policy Review: Insurance policies are often complex, filled with jargon, exclusions, and conditions. An attorney can carefully review all relevant policies—life, health, auto, home, disability—to understand your coverage, identify potential benefits, and ensure all terms are met when filing a claim.

- Claim Submission: Submitting an insurance claim correctly and promptly is crucial. A lawyer can assist in preparing and filing claims, ensuring all necessary documentation is included and deadlines are met. This minimizes the chance of delays or denials based on procedural errors.

- Bad Faith Denials: Unfortunately, some insurance companies may deny valid claims or offer inadequate settlements. An attorney can challenge these “bad faith” denials, negotiating fiercely on your behalf or pursuing legal action if necessary to compel the insurer to honor their obligations.

- Settlement Negotiations: In personal injury cases or property damage claims, an attorney will handle all settlement negotiations with insurance adjusters. They have the expertise to value your claim accurately and will fight for fair compensation, preventing you from accepting a low-ball offer that doesn’t cover your true losses.

- Contractual Obligations: A crisis can impact existing contracts, such as employment agreements, business contracts, or rental agreements. A lawyer can review these contracts to assess the impact of the crisis on your obligations and rights. They can advise on clauses like “force majeure,” which may excuse performance due to unforeseen circumstances, or help renegotiate terms.

- Force Majeure: This clause, often found in contracts, specifies circumstances (like natural disasters, pandemics, or other “acts of God”) that may relieve parties of their contractual obligations. An attorney can determine if a crisis falls under a force majeure clause and advise on the proper steps to invoke it, protecting you from breach of contract claims.

For comprehensive legal support in handling insurance claims, contract reviews, and other critical post-crisis legal needs, seeking out experienced legal counsel for personal injury cases is a wise decision. Their expertise can help you steer these often-contentious areas effectively.

Frequently Asked Questions about Legal Guidance After a Family Crisis

Navigating the aftermath of a family crisis often leads to many questions, particularly concerning the legal aspects. Here, we address some of the most common inquiries families have when seeking legal guidance after crisis events.

How much does it cost to hire a lawyer for a family crisis?

The cost of legal representation can vary significantly depending on the type of crisis, the complexity of the case, the lawyer’s experience, and their fee structure. It’s important to discuss fees upfront during your initial consultation.

- Contingency Fees: Common in personal injury and wrongful death cases, a contingency fee means the lawyer only gets paid if you win your case. Their fee is a percentage of the final settlement or award (typically 33% to 40%). This allows individuals to pursue justice without upfront legal costs.

- Hourly Rates: For estate planning, probate, guardianship, or other non-litigation matters, lawyers often charge an hourly rate. These rates can range widely based on location and experience. You will also be responsible for additional costs like court filing fees, expert witness fees, and administrative expenses.

- Retainers: Some lawyers may require an upfront retainer, which is a sum of money paid into a trust account from which the lawyer’s hourly fees and expenses are drawn.

- Free Consultations: Many personal injury and estate law firms offer free initial consultations. This is an excellent opportunity to discuss your case, understand your legal options, and inquire about fee structures without financial commitment.

- Case Complexity: The more complex the legal issues, the more time and resources a lawyer will need, which can impact the overall cost. For instance, a contested will typically costs more than an uncontested probate.

We always recommend getting a clear understanding of all potential costs and fees in writing before engaging a lawyer.

How long do I have to file a lawsuit after an incident?

The time limit for filing a lawsuit is known as the statute of limitations, and it is one of the most critical legal concepts to understand. These deadlines vary significantly based on:

- Varies by State: Each state has its own specific statutes of limitations for different types of claims. For example, the time limit for a personal injury claim in one state might be two years, while in another, it could be three or four.

- Varies by Claim Type: The deadline depends heavily on the nature of the crisis.

- Personal Injury: Claims arising from car accidents, slip and falls, or other injuries typically have a statute of limitations ranging from one to six years, with two or three years being common.

- Wrongful Death: These claims often have a similar, but sometimes distinct, statute of limitations compared to personal injury, usually two to three years.

- Medical Malpractice: These deadlines are often shorter and more complex, sometimes involving a “findy rule” where the clock starts when the injury is finded or reasonably should have been finded.

- Contract Disputes: Breach of contract claims usually have longer statutes of limitations, often four to ten years.

- Probate/Will Contests: There are strict, often short, deadlines for contesting a will or challenging aspects of probate, sometimes as short as a few months after the will is admitted to probate.

- Findy Rule: In some cases, particularly those involving latent injuries or fraud, the statute of limitations may not begin until the injury or wrongdoing is finded, or reasonably should have been finded, rather than the date of the incident itself.

- Tolling: Certain circumstances can “toll” or pause the statute of limitations, such as the victim being a minor or mentally incapacitated at the time of the incident.

Missing the statute of limitations can result in the permanent loss of your right to pursue legal action, regardless of the merits of your case. Therefore, seeking legal guidance after crisis events as soon as possible is paramount to ensure all deadlines are met.

What should I avoid doing before speaking with an attorney?

In the stressful aftermath of a crisis, it’s easy to make mistakes that could inadvertently harm your legal position. To protect your rights, it’s crucial to be cautious about certain actions before consulting with an attorney.

- Signing Documents: Do not sign any legal documents, waivers, or settlement offers from insurance companies or other parties without having your attorney review them first. These documents often contain language that could waive your rights or limit your ability to seek full compensation.

- Giving Recorded Statements: Insurance adjusters, especially those representing the at-fault party, may ask you to provide a recorded statement. Politely decline and inform them that your attorney will contact them. Recorded statements can be used against you later, even if you believe you are being truthful.

- Admitting Fault: Never admit fault for an accident or incident, even if you think you might be partially responsible. Liability is a legal determination that should be made by professionals after a full investigation. Any admission of fault can severely undermine your claim.

- Posting on Social Media: Be extremely careful about what you post online. Anything you share on social media—photos, videos, comments, status updates—can be accessed by opposing parties and used as evidence against you. Even seemingly innocuous posts could be taken out of context to suggest your injuries are not as severe as claimed, or that you are engaging in activities inconsistent with your recovery. It’s best to refrain from posting about the incident or your condition altogether.

- Delaying Medical Treatment: If you’ve been injured, seek medical attention immediately, even if your injuries seem minor. Delaying treatment can not only jeopardize your health but also allow opposing parties to argue that your injuries were not caused by the incident or are not as severe as you claim. Follow all medical advice and attend all appointments.

By exercising caution and seeking professional legal advice promptly, you can ensure that your actions do not inadvertently compromise your ability to secure justice and fair compensation.

Conclusion: Moving Forward with Legal Confidence

Experiencing a family crisis is undoubtedly one of life’s most challenging journeys. The emotional toll can be immense, often leaving us feeling vulnerable and overwhelmed. Yet, amidst the turmoil, the need for clear, decisive legal action becomes critically important. Ignoring the legal complexities can lead to prolonged distress, financial instability, and missed opportunities for justice.

Throughout this guide, we’ve emphasized the importance of timely action, from securing essential documents and assets to notifying key institutions and understanding the specific legal challenges posed by different crisis scenarios. We’ve highlighted how a sudden death can plunge families into the intricacies of probate and estate administration, while a serious accident demands meticulous attention to insurance claims and liability. Similarly, the incapacitation of a loved one brings forth urgent questions about powers of attorney and guardianship.

In each of these situations, the role of experienced legal counsel is not merely beneficial—it is often indispensable. A skilled attorney serves as your unwavering advocate, protecting your rights, offering objective advice when emotions run high, and expertly navigating the complex legal and contractual landscapes. They are instrumental in ensuring that your family’s best interests are represented, whether through negotiation, litigation, or meticulous adherence to court procedures.

By understanding the common pitfalls, such as signing documents without review or inadvertently admitting fault, and by being aware of critical deadlines like statutes of limitations, you empower yourself to make informed decisions. Engaging with legal professionals not only helps resolve immediate issues but also lays a solid foundation for your family’s long-term recovery and stability.

Moving forward after a crisis requires resilience, support, and, crucially, sound legal guidance. By taking proactive steps and entrusting the legal complexities to experienced hands, you can steer these challenging times with greater confidence, securing your family’s future and beginning the essential process of rebuilding after loss.